6 min read

A Case for Snap to Reach Valuation of $80 b

Snapchat has become a darling of teens and yet its parent Company Snap is facing skepticism from investors ahead of its planned IPO this week. The investors certainly have plenty of reasons to be ambivalent including the slowing user growth rates, competition, lack of voting rights, and of course the most important one, the valuation. However, I believe that Snap has a credible case to be an $80 b company, for the following reasons:

Snap has created an innovative content delivery model (Stories) that is efficient and fun to use for consumers while exceedingly well-suited for sponsored ads

Advertiser are moving to mobile platform and there are very few places they can reach consumers in this way- Snap can capture a good share of $ 94 b mobile advertising in 2017

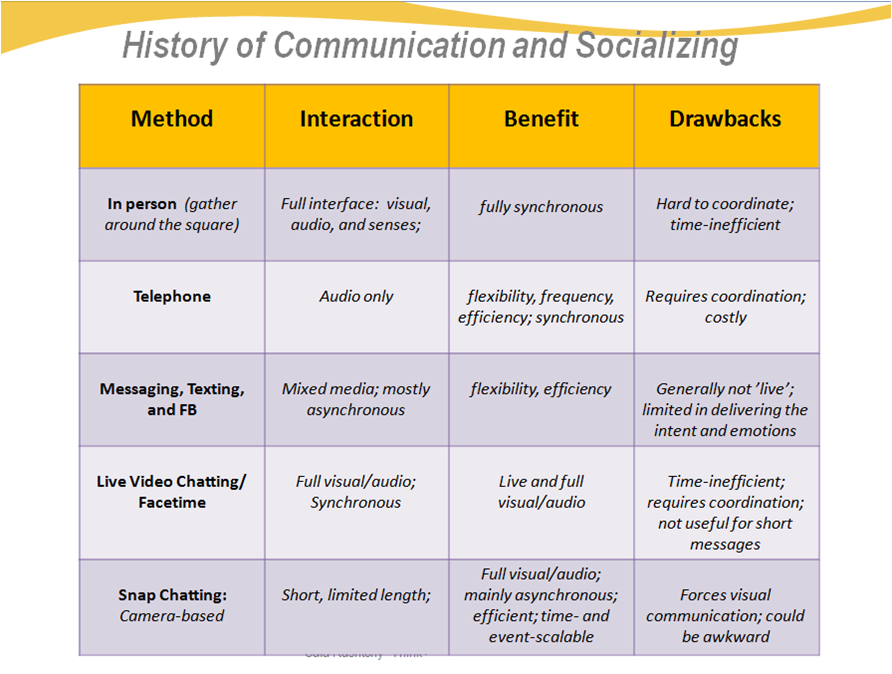

Snap’s camera-based communication model is an evolution in the communication paradigm (see chart below) that has appealed highly to millennials and has a chance to have wider acceptance by other demographics

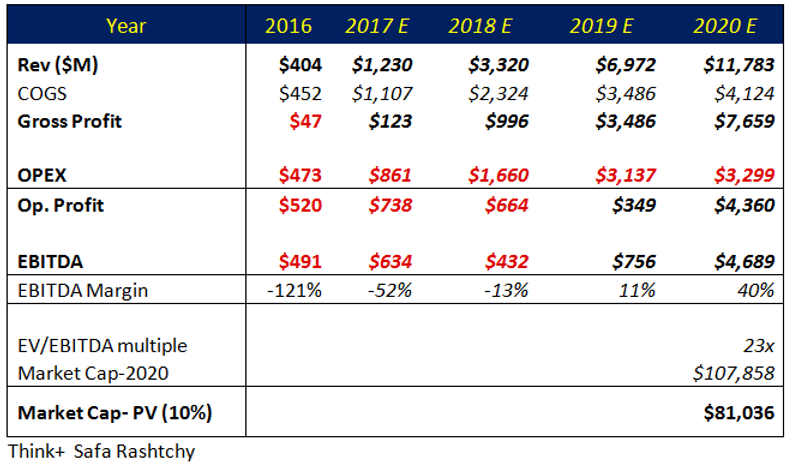

Snap’s revenues can grow from $1.2 b in 2017 to over $11.7 b by 2020, when it can create almost $5 b in EBITDA, making the company worth at least $80 b in 2017.

How Much Money Can Snap Make? This is of course the central question for Snap’s valuation, and it depend entirely on the level of acceptance by user for its communication and content delivery platform. Based on the arguments I will present below, I believe Snap’s user base can grow rapidly and reach 650 m DAUs by 2020. This will allow Snap’s revenue to reach $11.7 b, generating an EBITDA of $4.7 b. Applying a multiple of 22-23x on this (reasonable for the stage of growth the Snap will have then) and discounting the valuation by 10% per year gives 2017 valuation of $81 b.

There are of course multiple risks to achieving this, beyond lack of user growth. These include the increase in ARPU from the current levels to around $18 by 2020 (FB’s 4Q16 ARPU in the U.S. was $19.3) and overall expense level that can afford Snap a 40% EBITDA margin by 2020 (FB’s 4Q16 EBITDA margin was 58.3%). Below are my projections and the assumptions for Snap for the next few years.

Snap’s Big Hidden Value: A New Content Delivery Platform. Snap offers sponsored and curated stories including many by established content creators like CNN, WSJ and others. These stories are snippets of curated content, by the editors of these publications, that contain video and sounds and a short message that conveys the main storyline. As such, these stories are highly efficient way to deliver the content, and fun to watch. In an era where people have much shorter attention span, the ability to delivery personalized content in this way becomes very valuable. This is what Twitter was promising but failed to deliver. In many ways, Snap stories can be viewed as Twitter 2.0.

There is another major advantage for Stories: they are a natural format for delivery relevant advertisements since they allow the advertisers both to sponsor these mini-content as well as show their messages within the stories. This is at the heart of a bigger trend in advertising, where consumers are turning away from any ‘traditional’ format that are imposed over a content Even Facebook and Google are at a disadvantage with the current trends in advertising as their ads are still seen intrusive and consumers prefer to skip or block them. The only way for advertising to work is if the consumers see the value behind having the advertiser as part of the content, thus allowing the advertisers to reach the consumers heart and mind. Snapchat is uniquely positioned to take advantage of this trend.

Snap’s Core Value. Snap has quite possibly hit on the next wave of communication and content consumption. While Facebook and Instagram are used to post pictures and ideas and essentially seek approval and praise while communicating with your friends, Snapchat is used to primarily communicate in a new way, by capturing a short moment of your life. The images and videos are neither saved nor meant to get any “likes” or other reactions.

Thus, Snapchat is a communication tool more than a social network. Its primary use started with communicating with your closest friends using the camera and later with additional lenses and filters. In this sense, it competed more with messaging apps like WhatsApp, Viber, Line, etc. However, it offered a novel way to communicate that allowed, and in fact encouraged, goofy messages. Snap allows people to share their moment without being judged about it. Snapchatting was a real-time sharing of the moment, rather than posting an experience with the expectations of approval from others.

To the teenagers who were trying to find the most interesting and unusual emoji to send in their texts, this was a godsend. To the rest of us, Snapchat was a hard-to-use gimmick used by teens, mostly for sexting. But it gradually became obvious that Snapchat had hit on a new way to communicate that can potentially go beyond teens and goofy messages: instead of text or voice using pictures and videos, in a new way. ‘Snaps’ are quick to create, even quicker to watch, and highly efficient because they could convey the entire message in 10 seconds, and don’t require the other party to be on at the same time (they are asynchronous). The chart below shows the evolution of the communication platform and where Snapchat fits.

In some ways, Snapchat did to pictures and videos what Twitter tried to do with text communication, but eventually failed to gain wide acceptance. Similar to the Stories, Snap’s new communication mode is perfect for advertising revenues with its Sponsored Creative Tools (lenses, geofilters) that allow the advertiser to be part of the user’s content creation process.

Snap for Everyone? Ultimately, Snap’s success will depend on if this new mode of communication takes off beyond its current demographics. I think it is a fair bet that it can become the new mode, but only if Snapchatting proves to be efficient and comfortable enough for most types of communication, not just fun and youthful chatting. This requires further innovation from Snap, beyond their current lenses and filters. Among other things, the platform needs to become intuitive and much easier to use. While Snap’s success is not going to directly take people away from other platforms such as Instagram or Facebook, it will take away some of the available time from people and could eventually impact the usage pattern of other platforms.

Can Competition Outdo Snap? There are other advantages to Snapchat’s platform that can’t be duplicated by FB or Instagram. Snapchat appeals to its users because it allows them to escape from the news and sometimes depressing posts in Facebook. At the risk of some exaggeration, one can say that Facebook has become a way to show off your moment, get entertained by voyeurism, and yes, get some news (including sometimes even real news). This doesn’t mean FB lacks a legitimate and useful role in the daily lives of people, but it does mean that it lacks the legitimacy to launch a Snapchat model that can succeed. Similarly, Instagram is a feed format of getting entertained by pictures from your friends and celebrities you follow. It is also important to note that Snap has been the most innovative company during its first few years. It took Facebook many years before there was any meaningful innovation in its consumer-facing platform. Twitter is still struggling with this, while Snap has introduced dozens of game-changing features in just two years.

Risks. The case for $80 b valuation, even in the best-case scenario, is still heavily dependent on the execution of SNAP in the next two quarters, as well as investor sentiment which will govern the multiple on 2020 or other future year EBITDA. But most crucially, however, it rests on the assumption of SNAP reaching the monetization levels of around $18 ARPU (yearly average) by 2020. As an example of the sensitivity to ARPU, if SNAP were to get to say $8 ARPU, the discounted valuation will be cut back to $35 b. If, in addition to lower ARPU, SNAP’s DAUs grew to only 400 m by 2020, the valuation will be $22b. The factors that can cause these risks to materialize include lack of acceptance by broader demographics to use Snapchat (a major risk), insufficient content partners creating Stories, diminished user interest in watching Stories or accepting the imbedded ads, and lack of progress in increasing ARPU due to limited number of advertisers who can take advantage of the SNAP format (also a major risk).

Stay Connected

Receive our occasional thought pieces and insights.